As the market tightens, improving the digital experience for customers is rising to the top of the agenda for wealth managers. A majority of 86% of wealth management firms believe digital is a key priority ahead of the coming year, and are currently implementing at least one digital initiative.

Economic and geopolitical headwinds are having a major impact on the performance of the UK’s private wealth portfolios at the end of 2022. As inflation and the weak pound combined to hammer people’s buying power, UK wealth management portfolios lost about 10% on average – with some haemorrhaging as much as one-third – in the year to the end of September, according to research by Asset Risk Consultants (ARC).

Amid this chaotic environment, the work of wealth management firms has taken on an added importance, as clients ask how they will position themselves to preserve value in the coming months. According to a new study from financial services expert Alpha FMC, many entities in the sector are betting on the continued rush for digital to assuage their panicking customers – though legacy technology challenges continue to present them hurdles to that end.

Some 86% of firms now view digital is a top or high priority – and every single firm surveyed told Alpha FMC it was currently implementing at least one digital initiative. Meanwhile, 50% of firms were investing more than 10% of operating expenditure in digital – even as many businesses look for areas to save on spending amid the economic downturn.

“We might have expected to see digital progress and investment stall in this year’s survey, against the backdrop of the pandemic, geopolitical instability and a cost-of-living crisis” said Kenn Taylor, Alpha FMC’s Head of Wealth Management. “However, what we have witnessed is a digital change agenda that is not only very resilient but is in actual fact growing.”

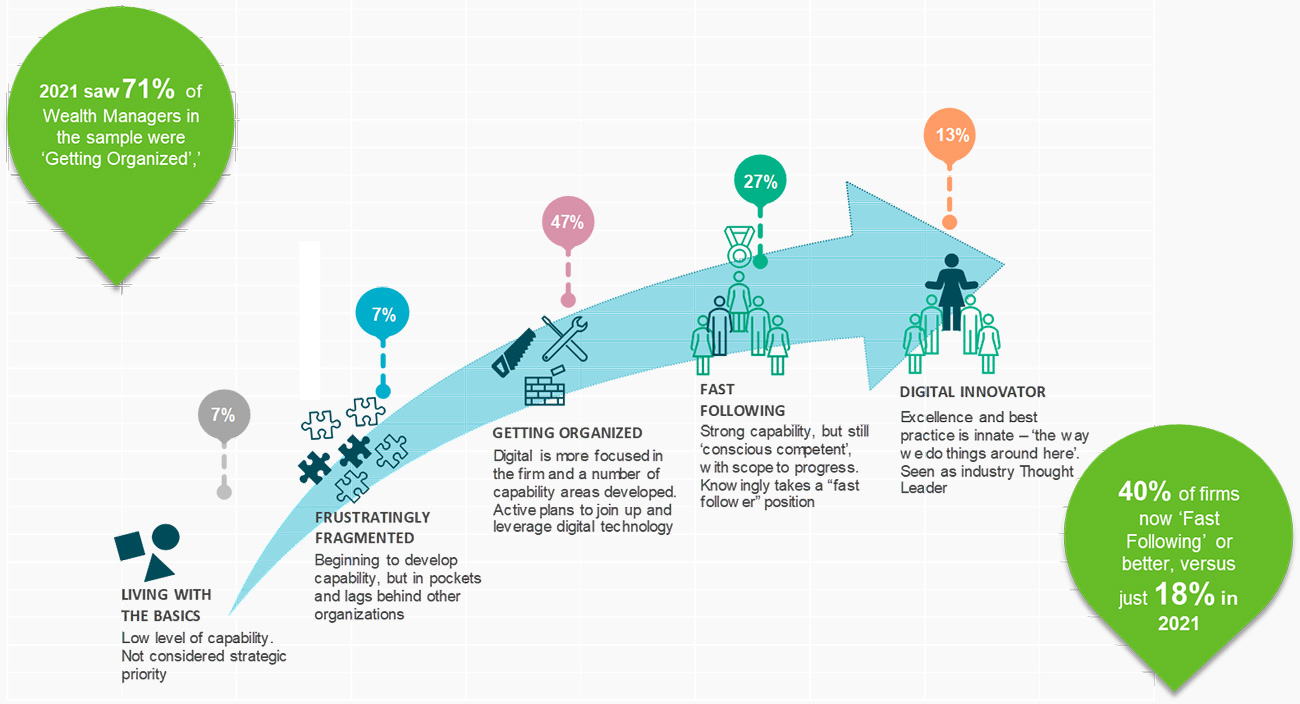

Wealth managers are doubling down on digital spending, with the hope of not only weathering the economic storm, but coming out ahead in a future recovery phase. Around 40% of firms now declare themselves as ‘Fast Followers’ or better, in comparison to 18% last year – demonstrating the new alignment in the sector on how important this is. In that regard, even one of the biggest historic headwinds to success, internal adoption, is being overcome with over 60% of RMs showing a very high uptake, and where trading is available, more than half of firms see very high activity.

That is not to say that there are no more challenges to digital progress in the sector, though. Over half of the wealth managers surveyed by Alpha FMC were using multiple operating models and technology capabilities, whether they operated across one or many jurisdictions. This is hampering progress in terms of taking on new technology, and agile working methods, as the complex or outdated architecture, and a fragmented supplier landscape make rapid change more difficult.

Meanwhile, many organisations also face the same old problem relating to data: if you put garbage in, you inevitably get garbage out. Any solution, however advanced, can only be as good as the data that ‘fuels’ it, and this is becoming more apparent to companies as their solutions improve. As a result, the number of respondents listing unreliable data as a major issue increased in Alpha FMC’s ranking of challenges to digital delivery, from 5th to 2nd over the last three years.

Taylor concluded, “As clients’ digital expectations continue to grow, we are seeing an ever-increasing focus of Wealth Management firms on their underlying technology and data capabilities; and with even their RM’s becoming advocates, the need to create a robust and scalable digital platform has never been greater.”